How to Improve Credit Score 100 Points Fast

A surprising number of Americans are just one credit score jump away from saving thousands of dollars. A person with a 620 score might pay dramatically more for a car loan than someone with a 720 score — even if both earn the same income. That’s why searches for how to improve credit score 100 points have exploded across the United States, especially among renters, first-time homebuyers, and people trying to escape high-interest debt cycles.

Most guides treat credit improvement like a willpower problem. They’re missing the real issue. Timing matters. Credit utilization thresholds matter. Even the specific day your card issuer reports your balance to the bureaus can move your score faster than months of careful payments. Think of your credit score like a financial GPA — small, strategic changes in the right categories move the average far faster than random effort scattered everywhere.

By the end of this guide, you’ll know exactly which actions produce the fastest measurable gains, which common mistakes quietly stall progress, and how Americans are realistically achieving 100-point credit score improvements in as little as 60 to 90 days.

How to Improve Credit Score 100 Points: Quick Answer

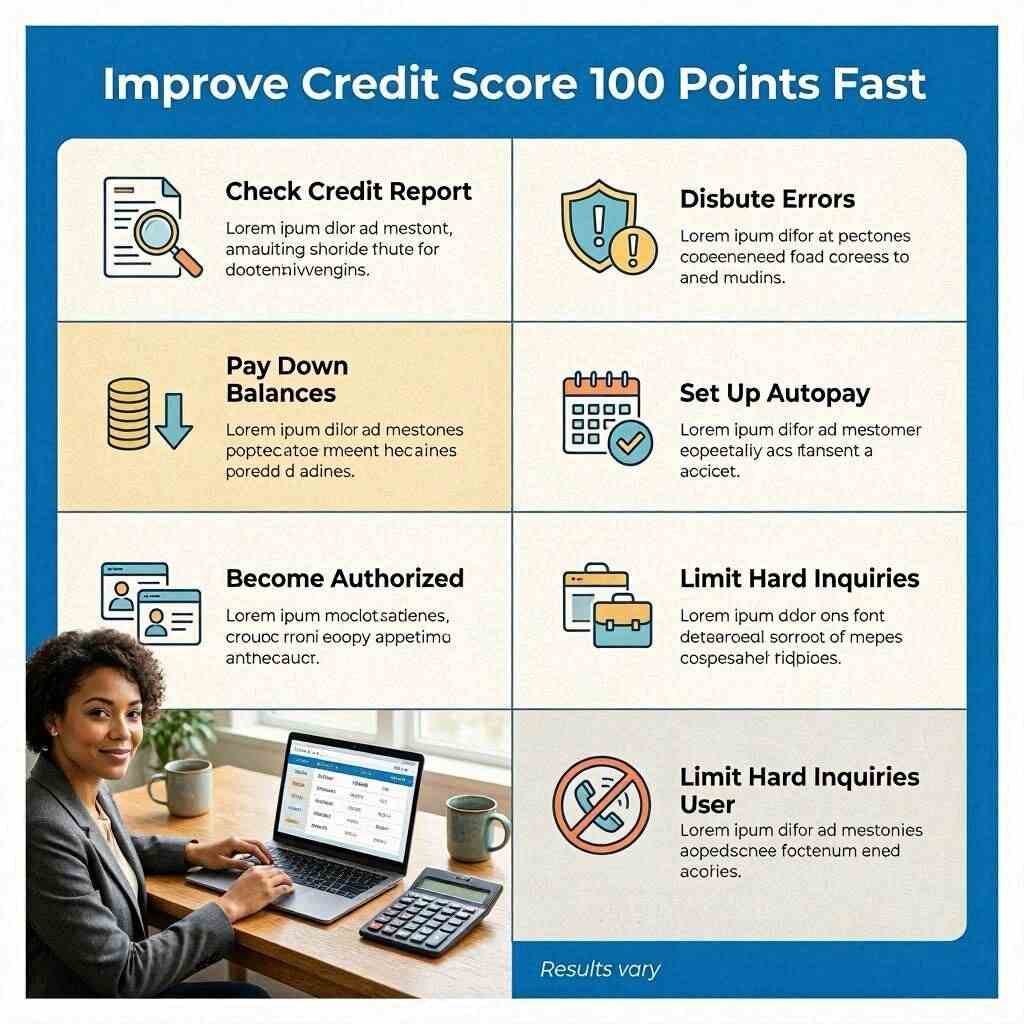

The fastest path to improving your credit score 100 points starts with lowering credit utilization below 10%, paying every bill on time, disputing credit report errors across all three bureaus, avoiding new hard inquiries, and strategically using tools like authorized user accounts, secured credit cards, or credit builder loans. Most Americans see measurable score gains within 30–90 days when they combine multiple strategies simultaneously rather than tackling them one at a time.

Understanding How Credit Scores Actually Work

Credit scores follow predictable patterns — they just aren’t explained clearly. Once you understand the underlying logic, improvement becomes far more strategic than emotional.

What a Credit Score Actually Measures

At its core, your credit score measures one thing: how risky lenders believe you are. Banks want to predict whether you’ll repay borrowed money consistently and on time. Every factor in the formula connects back to that single question.

Payment history carries the heaviest weight — roughly 35% of a standard FICO Score, according to FICO’s own published breakdowns. Miss one payment by more than 30 days, and the damage arrives faster than most people expect. A single late payment can behave like a bowling ball dropped on thin ice: sudden, disproportionate, and hard to undo quickly.

Credit utilization — how much of your available revolving credit you’re actively using — is the second major force shaping your score. When cards approach their limits, lenders read that as a sign of financial strain, even when every payment shows up on time.

Why Credit Scores Carry So Much Weight in the US

Beyond loan applications, your credit score quietly shapes everyday life in ways many people don’t fully register. Landlords check it before signing leases. Auto insurers in many states factor it into premiums. Utility companies sometimes require deposits based on it. Mortgage lenders make decisions worth hundreds of thousands of dollars based on three-digit numbers.

Picture two people financing the same $35,000 SUV in Texas. One carries a 640 credit score; the other has a 740. According to Federal Reserve consumer lending data, the lower-score buyer could pay thousands more in interest over a five-year loan term — same car, same economy, fundamentally different financial reality.

A 100-point score improvement, then, isn’t about pride or financial virtue. It’s about creating cheaper access to the things most Americans need anyway.

The Difference Between FICO and VantageScore

Plenty of Americans check scores through apps like Credit Karma, then get blindsided when mortgage lenders pull different — sometimes significantly lower — numbers. The reason is straightforward, even if no one explains it up front.

FICO and VantageScore use different scoring formulas. Both analyze similar behaviors, but they weight factors differently and treat certain account types distinctly. Mortgage lenders overwhelmingly rely on specific FICO models — FICO 2, FICO 4, and FICO 5 — while many free consumer apps display VantageScore 3.0.

Which Score Most Lenders Use

Conventional mortgage lenders in the United States primarily pull FICO scores from all three bureaus, then use the middle score for qualification decisions. Auto lenders and credit card issuers often work with their own proprietary FICO variations. If a mortgage is in your near future, monitoring your actual FICO Score through MyFICO.com shows you the number lenders will see — not an approximation of it.

Why Scores Vary Across Apps and Bureaus

Experian, Equifax, and TransUnion each maintain their own separate file, and creditors don’t always report to all three at the same time. One bureau might already reflect a recent balance payoff while another still shows the older, higher balance. Score fluctuations of 10–30 points across apps and bureaus are completely normal — not a sign anything is wrong.

The productive habit is watching for sustained upward movement over weeks and months. Daily number-checking is mostly noise.

💡 Pro Tip: Pull your full credit reports from all three bureaus at AnnualCreditReport.com before starting any improvement plan. Errors appear on one bureau without affecting the others, and catching a single inaccurate collection account can produce faster gains than months of behavioral changes.

The Biggest Factors Affecting Your Credit Score

Some ingredients dominate the recipe. Payment history and utilization together account for roughly 65% of a standard FICO Score — account age, credit mix, and new inquiries divide the remaining third between them.

Payment History Explained

Late payments are particularly brutal because they don’t just signal a cash flow problem — they signal unreliability. A single 30-day late payment can remain on all three bureau reports for up to seven years, with its sharpest impact in the first two years after it occurs.

There’s also a counterintuitive wrinkle worth knowing: the damage from a late payment depends heavily on your starting score. Consumers with excellent credit often lose more points from a single missed payment than someone already sitting at 580. Scoring models penalize deviations from clean behavior more aggressively, because they represent a departure from an established pattern. A California nurse with a 790 score who accidentally misses one credit card payment after switching banks could see her score drop more than 80 points. The same mistake hits a lower-score consumer less dramatically, precisely because there’s less clean history to protect.

⚠️ Common Mistake: Many people believe that paying the minimum amount immediately after missing a due date protects their score. It doesn’t. Once an account becomes 30 days past due and the creditor reports it, the damage is already done. The only real remedy is time, combined with consistent positive history from that point forward.

Credit Utilization Ratio

Of all the levers available, credit utilization moves fastest — and most Americans severely underestimate how much it’s costing them.

If your total revolving credit limit is $10,000 and your combined balances total $8,000, your utilization sits at 80%. That number signals financial pressure to scoring models regardless of whether your payment history is spotless.

What makes utilization particularly interesting is how the model reacts to specific thresholds, not just the raw percentage:

- Above 75%: severe risk signal — significant score suppression

- Above 50%: meaningful negative impact begins

- Above 30%: moderate penalty kicks in

- Below 30%: improvement zone

- Below 10%: strongest scoring benefit for most consumers

- Near 0% on all cards: can occasionally backfire — keep at least one card with a small active balance

The jump from 31% to 29% can matter more to your score than dropping from 60% to 50%, because you’ve crossed a threshold the model evaluates specifically. The math isn’t linear — the system isn’t designed to be.

💎 Expert Insight: Credit card issuers report balances on statement closing dates, not payment due dates. Paying your balance before the statement closes means the bureau receives a lower reported balance weeks earlier than most people realize. This one timing adjustment — paying before closing, not before the due date — is among the most underused credit improvement techniques available to American consumers.

Length of Credit History

Older accounts build trust in a way new ones simply can’t replicate quickly. A long track record tells scoring models that you’ve managed credit across varying conditions — not just during a recent push to improve your numbers.

Why Old Accounts Matter More Than People Think

An unused credit card still contributes meaningfully if it carries a zero balance and doesn’t charge an annual fee that makes keeping it painful. It increases total available credit, which lowers overall utilization, and it preserves your average account age. Old accounts work like seasoned cast iron — the longer they remain in good condition, the more value they add without any active effort on your part.

When Closing Cards Backfires

Paying off a card and closing it feels like closure. Emotionally, that makes complete sense. Financially, it creates two simultaneous problems: total available credit drops immediately, and average account age erodes over time as that history falls away. Close a $10,000-limit card while your other balances stay the same, and your utilization ratio can jump overnight — sometimes by 10 to 20 percentage points — before you’ve done anything else differently.

🔑 Key Takeaway: Improving a credit score 100 points rarely requires 20 actions. It requires focusing hard on the factors scoring models weight most heavily — payment history, utilization, and account stability — and letting everything else follow.

The Fastest Ways to Improve Credit Score 100 Points

People who gain 100 points don’t necessarily work harder than people who gain 20. They sequence their actions more intelligently. The order and combination of moves matters as much as the moves themselves.

Pay Down Revolving Balances First

Because utilization refreshes every billing cycle, reducing card balances is the fastest-moving variable most consumers can actually control. If your cards are near their limits, your score is dragging unnecessary weight that targeted payoffs can remove relatively quickly.

Focus on the highest-utilization cards first — not the highest dollar balances. A card sitting at 94% utilization sends a worse signal than one at 35%, even when the raw dollar amounts are similar. Individual card utilization matters alongside total utilization; the model watches both.

A few tactics that most guides skim past:

- Pay balances before the statement closing date, not the payment due date

- Target under 10% on each card individually, not just your overall rate

- Leave a small balance (1–3%) on one card occasionally to show active, managed use

- Never let any single card exceed 29%, even when your overall utilization looks healthy

💡 Pro Tip: Full payoff isn’t the only path to meaningful improvement. Dropping a card from 87% to 28% utilization can still produce real score movement within one reporting cycle — often within 30–45 days.

Dispute Credit Report Errors Strategically

According to CFPB data, millions of American consumers carry at least one inaccuracy on their credit reports. Some errors are trivial. Others are genuinely score-suppressing and fixable in under 30 days.

Pull reports from all three bureaus and review carefully for:

- Balances listed higher than your actual current balance

- Accounts that don’t belong to you — common after identity theft incidents

- Duplicate collection entries for the same underlying debt

- Payment statuses marked as late when records show otherwise

- Derogatory marks that have passed the seven-year reporting window

Disputes go directly to each bureau through their online portals. Under the Fair Credit Reporting Act, bureaus must investigate within 30 days. When the error is clear and documented, resolution can remove score-suppressing marks faster than almost any behavioral change you could make.

Become an Authorized User on a Seasoned Account

Being added as an authorized user on a trusted family member’s older, well-maintained account can bring years of positive history onto your credit report — history you didn’t need to be there for. You inherit the account’s track record simply by being added.

A college graduate in Florida with a thin credit file might gain real scoring momentum by being added to a parent’s 12-year-old card with a $15,000 limit and a $400 balance. Suddenly that account appears on the graduate’s report, carrying a decade of clean payment history with it.

Worth noting: it runs both ways. If the primary cardholder carries high balances or a missed payment somewhere in their history, joining that account may hurt rather than help. Always review the account before agreeing.

Use Experian Boost for Thin Files

Experian Boost lets consumers connect bank accounts and add qualifying utility, phone, and streaming service payments to their Experian credit profile. For people with thin files — not enough credit history to generate a reliable score — even modest gains from this tool can matter.

For someone with an established credit history, the impact tends to be smaller. But for renters, younger consumers, or anyone building from a near-blank starting point, every documented pattern of reliable payment builds toward something.

Consider a Credit Builder Loan

Credit builder loans work differently from conventional borrowing. The lender holds the loan amount in a savings account while you make monthly payments. You receive the funds at the end of the term — typically 12 to 24 months — along with whatever interest accumulated. The mechanism that matters isn’t the cash; it’s the unbroken chain of on-time payments that gets reported to the bureaus month after month.

For consumers with damaged payment history, this creates a consistent stream of positive marks running alongside older negatives. Over time, the new record progressively outweighs the old one. CFPB research has found that credit builder loans increase average scores by 24–35 points for consumers with no existing debt — a meaningful boost from a relatively low-risk product.

Open a Secured Credit Card Strategically

A secured credit card requires a cash deposit that functions as the credit limit. It reports to the bureaus exactly like any standard card — the only meaningful difference is that approval is nearly guaranteed, giving access to people who’d be turned down for unsecured cards.

Best Practices for Secured Cards

The common mistake is opening a secured card, barely using it, and wondering why nothing changed. Low activity limits reporting value.

Pick one predictable monthly expense — a streaming subscription, gas — assign it to the card, and set automatic full-balance payments. Keep utilization below 10% every month. After 12 months of steady, positive reporting, many issuers will upgrade the account automatically and return the deposit. The account then continues aging, which is valuable on its own.

🔑 Key Takeaway: The fastest credit score improvements happen when consumers combine utilization reduction, error correction, and positive reporting behaviors simultaneously — not one at a time. Running all three in parallel compresses the timeline considerably.

How to Improve Your Credit Score 100 Points Before Applying for a Mortgage

No credit decision carries higher stakes than a mortgage, and none rewards preparation more generously. The difference between a 620 score and a 740 score on a 30-year loan can easily exceed $50,000 in lifetime interest — not a rounding error.

FHA loans — a common path for first-time buyers — require a minimum 580 score for 3.5% down payment eligibility. Buyers scoring between 500 and 579 may still qualify but must bring 10% down. Conventional loans backed by Fannie Mae and Freddie Mac generally require 620 or higher, though the most competitive interest rates tend to open up above 740.

If a mortgage application is 6–12 months away, sequence your preparation deliberately:

First: Pull all three bureau reports and dispute every inaccuracy right away. Mortgage lenders pull all three bureaus, and a single unresolved error on even one can trigger an adverse action or complicate underwriting.

Second: Reduce all revolving balances as aggressively as possible. Mortgage underwriters evaluate your debt-to-income ratio (DTI) alongside your credit score — driving down card balances improves both numbers simultaneously.

Third: Freeze all new credit applications for at least six months before applying. New hard inquiries and newly opened accounts both temporarily suppress scores, and mortgage lenders read recent credit-seeking behavior as a risk signal.

Fourth: Leave existing accounts open and active, even paid-off ones. Closing cards in the months before a mortgage application — something many homebuyers do thinking it tidies up their profile — often backfires in ways that are difficult to reverse quickly.

⚠️ Common Mistake: Many pre-homebuyers open retail credit cards or apply for auto loans in the months before their mortgage application, believing that more accounts signal financial health. Multiple new inquiries and recently opened accounts can actually read as financial instability to mortgage underwriters — the opposite of the intended effect.

Credit Score Improvement Timeline

| Action | Typical Timeline | Potential Impact | Difficulty | Best For |

|---|---|---|---|---|

| Lowering utilization | 30–45 days | High | Moderate | High card balances |

| Disputing bureau errors | 30–90 days | Moderate to High | Moderate | Inaccurate reports |

| Becoming authorized user | 30–60 days | Moderate | Easy | Thin credit files |

| Opening secured credit card | 3–6 months | Moderate | Easy | Rebuilding credit |

| Credit builder loan | 6–18 months | Moderate | Easy | Damaged payment history |

| Removing collections | 2–6 months | Moderate to High | Hard | Severe score damage |

| Payment history buildup | 12–24 months | High (cumulative) | Easy | Long-term rebuilding |

What Changes Can Help in 30 Days

Utilization moves fastest because balances update with every billing cycle. A renter in Chicago carrying 82% utilization across three cards may see measurable improvement within a single reporting period just by reducing balances — without doing anything else.

Error disputes can also work quickly when the inaccuracy is clear and documented. A duplicate collection account or a balance shown as overdue when records prove otherwise can often be resolved within 30 days, sometimes producing score recovery that would otherwise take years.

What Usually Takes 3–6 Months

New positive history needs multiple reporting cycles before scoring models treat it as an established pattern rather than an isolated data point. Secured cards, credit builder loans, and payment consistency all require time to accumulate the weight they eventually carry.

Removing collection accounts — whether through negotiation, pay-for-delete agreements, or goodwill deletion requests — typically involves 60–90 days of back-and-forth. Success isn’t guaranteed, and patience is required.

Long-Term Credit Building Strategies

The strongest credit profiles don’t get built in a quarter. They develop over years of keeping older accounts alive, diversifying credit types responsibly, and allowing positive history to simply accumulate. Short-term tactics create the initial jump. Long-term discipline sets the ceiling.

Step-by-Step Plan to Improve Credit Score 100 Points

A focused, 90-day improvement campaign doesn’t have to be complicated. It just has to be consistent.

Step 1: Pull All Three Credit Reports

Complete visibility comes first. Monitoring a single score app while ignoring bureau-specific discrepancies is one of the most common ways people stall their own progress. Review every account entry, every balance, every payment status across all three bureaus. One inaccurate derogatory mark can anchor your score like something heavy attached to a boat that would otherwise move freely — invisible until you go looking.

Step 2: Lower Utilization Below 10% on Every Card

Focus payoffs on highest-utilization cards first, and target under 10% per individual card — not just your overall combined rate. Scoring models evaluate both, and a single card sitting at 90% can drag your score even when everything else looks reasonable.

Remember the threshold effect: dropping from 31% to 28% may deliver more scoring gain than dropping from 60% to 35%, because you’re crossing a boundary the model specifically evaluates.

Step 3: Automate Every Payment Without Exception

A single missed payment can erase months of progress. Automation removes the human-error variable entirely — set autopay for at least the minimum due on every account, then make manual extra payments whenever cash flow allows. A contractor in New York juggling multiple client invoices each month may forget a credit card due date during a busy stretch. That one oversight could cost more points than six months of careful behavior gained. Automation makes that scenario impossible.

Step 4: Add Positive Reporting Channels

If your existing account mix is thin, open at least one additional source of positive monthly reporting. A secured card, a credit builder loan, or a rent-reporting service like Self, Boom, or Rental Kharma can all contribute consistent on-time history without requiring meaningful new debt.

Step 5: Pause All New Credit Applications

Multiple hard inquiries in a short window signal credit-seeking behavior — and temporarily suppress scores regardless of whether applications are approved. If a major credit milestone is approaching, stop applying for anything else for at least six months beforehand and let existing positive history compound undisturbed.

Step 6: Monitor Progress Monthly

Score movement isn’t linear. Fluctuations of 5–15 points week to week are normal — the system is updating, not malfunctioning. What to watch instead: utilization trending down, negative marks aging off, on-time payment streaks growing, accounts getting older. Monthly review catches real progress. Daily checking mostly creates anxiety.

Common Credit Score Mistakes to Avoid

Progress often stalls not because people are doing the wrong things, but because they haven’t stopped doing things that quietly pull in the opposite direction.

Closing Old Credit Cards After Paying Them Off

Paying off a card and closing it feels like a clean ending. The financial reality is less tidy. Older accounts strengthen average account age and contribute to total available credit. Closing them removes both advantages at once. In most cases, a paid-off card with no annual fee is worth keeping open indefinitely — even with zero balance and zero use.

Ignoring Statement Closing Dates

Payment due dates are widely understood. Statement closing dates — the date when issuers actually report balances to the bureaus — are not. Paying before the statement closes means the bureau receives a lower balance, potentially weeks before the due date ever arrives. This single timing adjustment consistently outperforms expensive credit repair services for consumers with high utilization and otherwise clean reports.

Applying for Multiple Cards in a Short Period

Opening several accounts quickly generates multiple hard inquiries, lowers average account age, and signals credit-seeking behavior to underwriting systems. More available credit does not automatically translate to a higher score — the timing, pattern, and quantity of new accounts matters as much as the resulting credit limits.

Ignoring Small Collection Accounts

A collection for $180 might not feel worth dealing with. But non-medical collections of any size can meaningfully suppress scores depending on which FICO model a lender uses. While CFPB guidance has reduced the impact of some medical debt in newer scoring models, older FICO versions — still widely used by mortgage lenders — aren’t as forgiving.

💎 Expert Insight: Consumers with lower starting scores often improve faster during an active campaign than high-score consumers do. Scoring models reward dramatic reductions in risk signals more aggressively — dropping from 580 to 680 is frequently easier to accomplish in a given timeframe than moving from 720 to 820.

People Also Ask: Credit Score Questions Answered

Can You Really Raise Your Credit Score 100 Points in 30 Days?

For some consumers, yes — but the starting conditions determine almost everything. Someone with multiple maxed-out credit cards, no missed payments, and clean bureau reports may see a 100-point gain within a single billing cycle simply by paying balances down below 10% utilization. Scoring models react immediately to utilization changes because card balances update every reporting cycle. Consumers dealing with recent missed payments, active collections, or bankruptcies typically need 6–18 months for comparable improvement.

Does Paying Off Debt Improve Credit Immediately?

Paying off revolving debt — credit cards, lines of credit — typically improves scores within one billing cycle once the lower balance is reported. Timing that payoff before the statement closing date accelerates the result. Paying off installment loans (auto loans, student loans) occasionally triggers a temporary small dip because of shifts in credit mix and active account count, though the long-term effect of carrying less debt is almost always positive.

Is Paying for Credit Repair Worth It?

Most of what credit repair companies do, consumers can do themselves at no cost: disputing bureau errors, negotiating with collectors, requesting goodwill deletion of isolated late payments, and optimizing utilization. Both the CFPB and FTC note that legitimate credit improvement takes time regardless of who does the work. Genuinely complex cases — identity theft recovery, extensive mixed-file disputes — may justify professional help. Routine improvement generally doesn’t.

What Is a Good Credit Utilization Ratio?

Below 30% is the standard recommendation, and it’s a reasonable floor. For consumers trying to maximize scoring benefit, staying below 10% on each individual card and overall produces the strongest results in most FICO models. Think of utilization like a stove dial — a little warmth is fine, but once the temperature climbs, scoring models read it as pressure regardless of whether anything is actually burning.

Can Rent Payments Build Credit?

Increasingly, yes. Services like Self, Rental Kharma, and Boom report rent payments to one or more major bureaus, letting renters build positive credit history without taking on new debt. Some landlords partner with reporting services directly. Experian RentBureau collects rental payment data that feeds into Experian reports specifically. Rent reporting delivers the most value for consumers with thin files — people who need more consistent positive reporting activity to generate reliable scores.

Frequently Asked Questions About Improving Your Credit Score

1. How long does it take to improve a credit score 100 points? It depends almost entirely on what’s suppressing your score. If high utilization is the primary problem, 30–60 days of focused paydowns can realistically produce 100-point gains. If missed payments or active collections are involved, a more realistic timeline is 6–18 months of consistent positive behavior. Running multiple strategies simultaneously — utilization reduction, error disputes, and new positive reporting — compresses the timeline significantly compared to sequential action.

2. What credit score is needed to buy a house? FHA loans require a minimum 580 score for 3.5% down, or 500–579 with 10% down. Conventional loans typically require 620 or higher. VA and USDA loans carry their own requirements. Most buyers see meaningfully better mortgage rates at 740 and above. Improving your score before applying directly reduces your total lifetime interest cost — often by tens of thousands of dollars over the life of a 30-year mortgage.

3. Does checking your own credit score lower it? No. Checking your own credit through any monitoring service or free bureau request generates a soft inquiry, which has zero impact on your score. Only hard inquiries — triggered when you formally apply for new credit — affect your score, and even those are typically small (5 points or less) and fade within 12 months.

4. How do I remove a collection account from my credit report? Three main avenues exist: dispute the account as inaccurate if it contains verifiable errors; negotiate a pay-for-delete agreement with the collector, where they remove the account upon payment; or send a goodwill deletion letter to the original creditor if the collection resulted from an isolated mistake within an otherwise clean history. None are guaranteed outcomes, but all are worth pursuing before the seven-year reporting window closes on its own.

5. Does a balance transfer affect your credit score? Balance transfers affect scores through several channels at once. Opening a new balance transfer card generates a hard inquiry and reduces average account age. At the same time, moving a large balance off a nearly-maxed existing card can dramatically reduce that card’s individual utilization, often producing a net positive score effect within one to two billing cycles. Keeping the original card open after the transfer preserves available credit and prevents a utilization spike on that account.

6. What is a credit builder loan and does it actually work? Credit builder loans are engineered specifically for score improvement. The lender holds the loan amount in a savings account while you make monthly payments for 12–24 months — each of which gets reported to the bureaus. At the end of the term, you receive the funds. CFPB research shows credit builder loans increase average scores by 24–35 points for consumers with no existing debt, making them a legitimate tool rather than a marketing gimmick.

7. Can medical debt hurt my credit score? Yes, though the picture has grown more complicated recently. CFPB regulatory changes removed medical collections under $500 from FICO 9 and VantageScore 4.0 calculations. However, older FICO models — including versions 2, 4, and 5 still used by most mortgage lenders — do count medical collections. For anyone preparing for a mortgage application specifically, any medical collection on any bureau report deserves attention regardless of the dollar amount involved.

8. How many credit cards should I have to maximize my score? No universally ideal number exists — the utilization, payment history, and account age across your cards matter far more than the count. Consumers with two to four cards, low utilization on each, and a clean payment history typically have excellent scores. Opening several cards quickly to increase available credit usually backfires: hard inquiries stack up, average account age drops, and the net scoring effect is often negative in the short term. Build slowly and intentionally.

9. Does a debt consolidation loan hurt your credit? Short term, a consolidation loan creates a hard inquiry and a new account — both slightly suppress scores temporarily. Over the following 60–90 days, if the consolidation meaningfully reduces utilization across multiple cards, scores typically recover and improve. Long term, the simplification of payment obligations tends to reduce the risk of missed payments, which benefits scores more than almost any other factor. The short-term dip is real; the longer-term trajectory is usually better.

10. What’s the fastest single action to improve a credit score? For most Americans, paying down credit card balances before the statement closing date — to bring utilization below 10% — produces the fastest single-action result. It takes effect within one billing cycle, requires no application, no new account, and no external cooperation. For consumers with bureau errors, filing a dispute on a clearly inaccurate negative mark is the second fastest option. Both actions can be initiated within a week and produce visible results within 30–45 days.

Advanced Expert Insights

The deeper you go into credit scoring, the more it behaves like a behavioral prediction engine than a straightforward math problem. That distinction matters when you’re deciding where to put your energy.

The Counterintuitive Reason Paying Off Debt Can Temporarily Lower Scores

Paying off an installment loan entirely can occasionally trigger a small, temporary score dip — and this surprises people who reasonably expect the opposite. Installment loans (auto loans, personal loans, student loans) contribute to credit mix diversity, one of the five components FICO evaluates. Removing the only installment loan from an otherwise credit-card-heavy profile can narrow that diversity slightly, causing a brief dip of 5–15 points. It’s temporary, and long-term, carrying less debt is always the right direction. Don’t let the possibility of a short-term wobble talk you out of paying off debt.

Why Utilization Thresholds Behave Non-Linearly

Scoring models appear to evaluate utilization at specific threshold crossings rather than along a smooth curve. Moving from 31% to 29% may produce a larger gain than reducing from 60% to 40%, because the former crosses a weighted boundary. Understanding where those thresholds fall — roughly at 75%, 50%, 30%, 10%, and near 0% — lets you target payoffs at the boundaries that return the most scoring benefit per dollar spent, rather than just attacking the largest balances.

The Future of Credit Scoring in America

Traditional credit data — loans and credit cards — is increasingly insufficient to capture the full financial behavior of millions of Americans. Alternative data points are making their way into lender evaluation frameworks: rent payments, utility history, banking cash flow patterns, subscription consistency. This shift is slow but accelerating.

Alternative Data and AI-Driven Lending

Over the next several years, lenders will increasingly factor in:

- Verified rent payment history through specialized reporting services

- Utility and telecom payment consistency

- Banking account cash flow patterns and income stability

- Subscription payment behavior as supplementary reliability signals

For the millions of Americans with thin traditional credit files — recent immigrants, young consumers, lower-income renters — this evolution could mean fairer access to credit than current FICO-only models allow. The consumers who build positive patterns across multiple payment types now will be positioned well ahead of that shift.

🔑 Key Takeaway: Credit scoring is moving toward a broader behavioral reliability model — not just debt management history. Establishing consistent positive patterns across multiple payment categories positions consumers well for both current and future lending environments.

Conclusion

Credit problems feel permanent when you’re inside them. They aren’t. Most Americans who achieve meaningful score improvements don’t do it through insider tricks or expensive services — they identify the few factors that carry the most weight, apply pressure there consistently, and let the system respond the way it’s designed to.

Two actions produce the fastest results for the widest range of people: reducing credit utilization below 10% before statement closing dates, and disputing any errors across all three bureaus simultaneously. Both can generate measurable changes within 30 to 45 days. Everything that follows — secured cards, credit builder loans, authorized user accounts, automated payments — compounds on top of that foundation.

Understanding when the system updates matters as much as understanding what to do. Statement closing dates matter. Utilization thresholds matter. Bureau-specific reporting discrepancies matter. These aren’t hidden tricks. They’re predictable features of a system built to reward people who understand how it works.

When you’ve been searching for how to improve credit score 100 points, the principle worth holding onto is this: gains compound. Lower utilization makes consistent payment history carry more weight. Corrected errors remove anchors that were dragging down a profile that might otherwise be recovering. Each improvement amplifies the others around it.

A stronger credit score doesn’t just change a number — it changes what that number costs you. Your mortgage rate, your auto loan, your insurance premium, your apartment options. Start with the highest-impact moves. Track progress monthly rather than daily. And know that the system responds more predictably than it looks from the outside.

💡 Pro Tip: Lead with utilization reduction and error correction — they move fastest. Add a positive reporting channel in month two. Let payment consistency compound from there. Three focused months of this approach can produce changes that take others years of passive, hopeful waiting.